Sundaram Clayton - Demerger Analysis

Sundaram Clayton - Demerger Analysis

This summarized article will focus on Sundaram Clayton which has recently announced demerger of its businesses into 2 subsidiaries & what the payoff looks like currently?

Estimated time to read - 6 minutes

About company –

Sundaram Clayton Limited was incorporated in Chennai in 1962 and is part of the TVS group, led by Mr. Venu Srinivasan. It is engaged in the business of manufacturing and distributing aluminum die castings. It also acts as a holding company for TVS Motors limited where it has 52%of TVS motors.

Aluminum Die Casting business -

The company manufactures aluminum pressure die castings for heavy commercial vehicles, passenger cars and two wheelers. The customers of this division are major automotive companies. The product range manufactured by company -

52% stake in TVS motors -

The company also acts as a parent of TVS motors which is valued at around 30,000 crores. TVS motors is engaged in manufacturing two-wheelers and its accessories; it currently manufactures a wide range of two-wheelers and three-wheelers.

This article is focused more towards finding holding company discount as majority (90%+) of the market value can be attributed to TVS motors stake. Hence the business prospects of TVS motor & Aluminum die casting haven’t been discussed in detail.

Recent announcement on 9 February, 2022 –

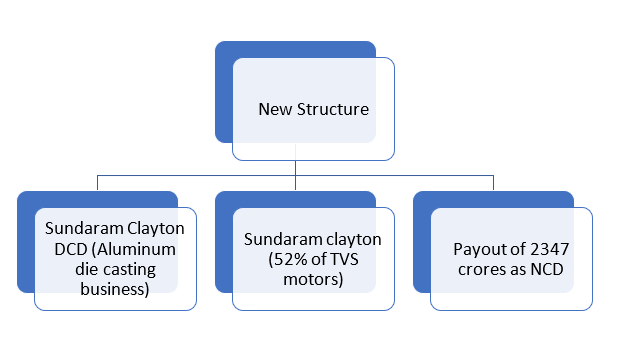

The company will demerge the Aluminum Die casting business into a new subsidiary Sundaram Clayton DCD & listed on the exchanges. The current Sundaram Clayton company will end with holding 52% of TVS motors. Also company had sold 5% of TVS motors & holds cash on balance sheet which will be paid out. The payout is estimated at Rs 2347 crore which will be paid out Non Convertible Debentures once the NCLT approves the transaction. 116 NCD of Rs. 10 each will be issued by company for each share held of Sundaram Clayton. The NCDS’s would be redeemed after 1 year of issuance. Essentially, the family wants to split their businesses & remove/ reduce cross holding in other companies.

New structure would be –

As the company would be demerged into 2 companies I have done Sum Of The Parts valuation method to arrive at Sundaram Clayton’s overall valuation -

Sundaram DCD (Die casting business) -

I have assumed 5% Net profit margin for the company analysis & 1000 crore annual revenue i.e. annual PAT of 50 cr.

Sundaram Clayton -

The current company will hold only TVS motors stake which is valued based on current market cap.

Sum Of The Parts Valuation -

2347 crores is the distribution that would be made to shareholders & hence is considered separately rather than being included in market cap of Sundaram Clayton.

How much holding discount is appropriate?

Here the quote from 2point2 article on holding company discount comes handy which states -

Prefer to invest at peak discount: We track the discounts of HoldCos over many years. The discount moves between a wide range. We prefer to invest when the discount is at its peak or higher than normal, to benefit from the discount narrowing over time. This also ensures that the dividend yield differential is higher than normal.

Based on historical data of prices of TVS motors & Sundaram Clayton from 1-4-14 to 26-2-22 the holding company discount chart looks like this -

The current discount 57% looks closer to the mean of 54% as on 26 Feb,2022. But, the situation might become investable in case the discount increases due to ongoing market depressed sentiments.

Final verdict -

Overall, the step is in the right direction by the promoters to demerge 2 different businesses. The holding company discount for Indian listed companies is usually in 40-60% range depending upon business models & capital allocation. Also, one needs to note that other lucrative opportunities too exist post the recent correction which has made the Sundaram Clayton Demerger play less relevant if it stays at current levels. If the discount rises to near A (marked in picture above) at 60-70% one might look to invest in the strategy given the expected payout.

What can go wrong?

Usual time for demerger is 12-16 months but it might take 24-30 months.

Company starts pouring money into Die Casting business rather than paying dividend.

Demerger is rejected by board of directors/ NCLT / shareholders due to change in market conditions.

Demerged company doesn’t get listed like Sintex. (Less probable case given TVS group corporate governance looks clean)

Missed an important point you know, please share in the comments section below.

If you liked the article, consider sharing the article & hit the subscribe button below.

Note -

In case you would like change the assumptions I have used in calculating payoff you can do it by downloading the sheet.

The article has been desperately cut short to sustain your attention span.

I am AMFI registered Mutual Fund Distributor . In case you have mutual fund queries or would like to invest in mutual funds, let me know on my Email - chirag.jain48@yahoo.com or +91-7567473055.

AMFI registration number - ARN-187955

Dear Chirag! Fantastic analysis , As you said in Feburary 2022, now we are in 26th March 2023, Picking holding Co. at discount of 58% in Feb 222 / Sundaram Clayton on Ex date 24th Mrch 23, Bonus NCPRS basis scrip 20% down, I feel another 20% down during the week possible. Similar your views I need to have from your end a rare amalgamation of Pressman Advertisements, where the Promoters holding alone complete erosion of / complete capital reduction of Promoters stake. A Suresh Babu

Now that it is all set for implementations of the scheme, shall request for fresh post DONE estimate for valuation of two entities.