Medium to Long Duration Funds - A Wise Theft

Medium to Long Duration Funds - A Wise Theft

MF shots (part 8)- is an exclusive series of article which will try to explain in each category of mutual fund. This article focuses on Medium to Long Duration funds which invest for 4-7 years.

Estimated time to read - 5 minutes

I am AMFI registered Mutual Fund Distributor . In case you have mutual fund queries or would like to invest in mutual funds, let me know on my Email - chirag.jain48@yahoo.com or +91-7567473055.

AMFI registration number - ARN-187955

Overview –

MF shots - name describes itself where Mutual Fund categories are explained in a brief manner to avoid clutter of information. The current article is continuation of MF shots series by Cellestial Wealth. Previously I have written about short term & medium term debt mutual funds of which can be found by clicking on each category. Each article takes less than 6 minutes but states a few key pointers to be looked upon when choosing a category.

Overnight fund – invests in securities with maturity of 1 day.

Liquid fund – invests in securities with maturity of 91 days.

Ultra short duration funds – invests in securities with maturity of 3-6 months

Low duration funds - invests in securities with maturity of 6 months to 1 year.

Money market funds - invest in securities with maturity upto 1 year.

Short duration funds - invest in securities with maturity ranging from 1 to 3 years.

Medium duration funds - invest in securities with maturity ranging from 3-4 years.

Brief –

In this category the fund managers invest with higher time horizon compared to short duration managers, which allows higher yield to be earned on their investments. The category has Rs. 14000 crore of AUM, which is currently low compared to equity mutual funds & short term debt mutual funds. The average expense ratio in the category is 0.83% which is high compared to category average in debt mutual funds.

Investment objective –

The objective is to invest for 4-7 years in a mix of corporate & government securities. Corporate securities help enhance yield of the portfolio with more risk than government security.

Suitable for which type of goals –

1. Children education fees due in next 4-5 years.

2. Goals with duration of 3-4 years.

Risk levels –

The risk is at high levels due to duration risk taken by funds i.e. they invest for 4-7 years. Also the returns have been comparable to short duration & medium duration funds albeit with higher risk levels.

What parameters to check –

1. Expense ratio –

High expense ratio reduces net returns for investor & matters even more when returns are lower in the debt mutual fund. It becomes worse when lower returns are earned over period of 4-7 years.

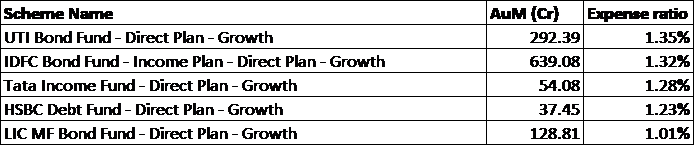

Below are funds with highest expense ratio -

2. Duration & yield of bonds held –

The fund manager might choose lower yielding government securities in pursuit of lower expense ratio, but it might become detrimental for investor as the net returns to investor might be much lower.

3. Portfolio manager –

The decision to weigh corporate & government security is done by manager & yield curve positioning a crucial return differentiator is also done by portfolio manager.

What to avoid –

1. Funds with expense ratio in excess of 1% -

Expense ratio lower are better. Give a careful look at it & monitor it even after you have invested in the fund.

2. Investing based on past returns -

In the recent years, there has been series of interest rate cuts which have enhanced the past 3 & 5 year returns for medium to long duration funds. But they will end up suffering if there is interest hike occurs in near future.

Interesting insights from category –

1. TATA Income fund has a has a higher expense ratio of 1.28% which might be due to higher holding of corporate security at 65% of portfolio .

2. A quarter of returns end being paid to the Mutual fund manager in direct category. Wondering what investors of regular plans earn?

3. Only 14 mutual fund schemes exist in this category reflecting lack of popularity.

4. Funds on average have 40-60 ratio of corporate & government securities respectively.

Conclusion –

The category can be looked upon if investor expects interest rates to reduce in future, which currently isn’t the case. The expectations are of stable/ rising interest rate regime & investing in this category currently doesn’t look a suitable choice. Also, the returns look sub-optimal compared to offered by alternatives post deduction of expense ratio. Hence one should adopt a wait & watch approach for this category to invest in it.

Finally, I have called this category a theft because the net returns of investor currently are below compared to offered by alternatives & are beneficial only to Asset Management companies. Therefore, one should only invest if suggested by financial advisor or one has sound knowledge & can time the yield curve movements.

Greetings of New Year to all readers. Will bring you something exciting in the new year. Stay tuned & hit the subscribe button below in case you haven’t.

Notes -

Top 10 funds by AUM -

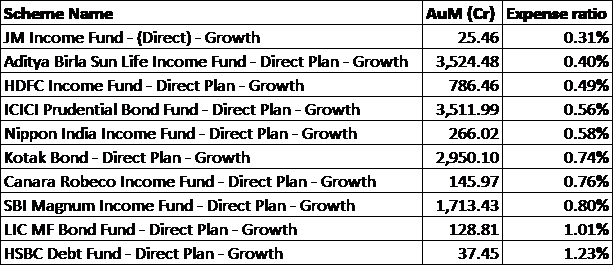

Top 10 funds by lowest expense ratio -

Full data sheet of funds can be accessed here.