Embassy Office Parks REIT - An Underdog?

Embassy Office Parks REIT - An Underdog?

This post is a deviation from usual ones where I discuss about mutual fund categories. This article is about Embassy REIT which was the 1st REIT to list on exchanges in India.

Estimated time to read - 15 minutes

Brief -

REIT (Real Estate Investment Trust) category is popular across the globe & used by many small & institutional investors to diversify & earn periodic income from it. In short term returns are volatile & similar to equity returns but in longer term the returns are more or less steady rather than volatile returns of equity market due to underlying cash flows being more predictable. In longer term they move in tandem with underlying real estate it holds. Below table represents historicalUS REIT index returns compared to US equity returns.

Industry

The real estate market varies highly amongst geographies. Each sub market (Bangalore, Kolkata, Hyderabad, etc.) have varying supply demand vacancies which drive the rental yield, vacancies & capital appreciation of properties. The supply of local talent & government incentives are key drivers for REIT industry.

For this article, only sub-markets of Embassy REIT (Mumbai, Bangalore, Pune & NCR) are considered.

Supply side of REIT industry -

Embassy REIT has explicit focus only on A grade properties. A grade properties are high quality office spaces which are sought by MNC’s & have lock in period with fixed escalations. Out of 120 Million Square Feet (MSF) supply expected only 13 MSF is potential supply in Embassy’s REIT market of NCR, Mumbai, Pune & Bangalore.

The demand side –

The demand side varies depending upon the leasing area coming up for renewal. Also, if a company wants to increase its area under lease or would downsize or leave the property. Usually MNC’s tend to be sticky unless there is change in company strategy or acquisition of company.

Company

Embassy REIT - Structure -

Embassy REIT holds multiple special purpose vehicle which have cash flow/ rent generating properties as assets. Initially the REIT lends money to SPV which builds assets over time & when these properties start generating cash flows these are transferred to REIT equity owners as dividends, interest or capital repayment to optimize tax efficiency. Below infographic represents the movement of funds within the REIT.

Assets/ Properties held -

The REIT valuation is defined by properties held. Below is breakup of property held & potential development that can be done on its existing land bank held.

The properties majorly (90%+) consist of A grade office spaces & rest contributed from Hotels and energy plant. The office property generates rent which is received by SPV & transferred to REIT as capital repayment, interest & dividend to reduce taxes for investors (as reflected in above chart).

The hotel revenue consists of revenue from Food & Beverage & room rents. The revenues are split between operator (i.e. Hilton or Four Seasons) & rest is transferred to the REIT. Hence one needs to note that the operational risk is shared by shareholder of REIT rather than occupier (Hilton or Four season).

Embassy energy is a 100 MW solar plant which supplies energy to Embassy’s office parks in Bangalore at pre-determine prices which is collected from tenants.

The total asset value of all assets combined as on 30-9-21 is 46,750 crore (Source – corporate announcement) & debt of 18,160 crore leading to NAV of 37,000 crore .

Company earns 74% of its revenue from Bangalore & the rest from Mumbai(9%) , Pune (10%) & Noida(7%) . Top 10 occupiers contribute 38% to gross rentals (source – company) with no occupier exceeding 10% of rentals.

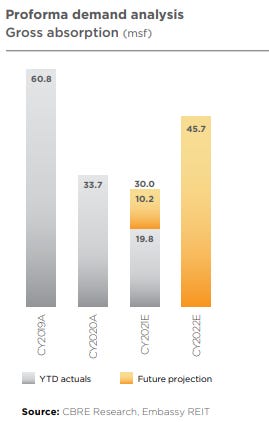

How covid affected Embassy REIT ?

The company was able to collect rents from its marquee clients with 99% efficiency but as agreements came up for renewal some occupiers quit along with fresh demand collapsing. Earlier(pre-covid) company used to lease out 1 Million Sq. Ft. (MSF) per quarter due to strong but post covid it was reduced to half (0.5MSF/ quarter). Due to uncertainity, the demand from occupiers fell affecting new leasing & re-leasing activity (i.e. when one tenant leaves & property is leased out to other one). The higher vacancy affected the value of office property leading to lower NAV.

For hotels space - the valuation was based on average occupancy of hotel & average room revenue per night. Due to covid it took a backseat affecting valuation of hotel property.

For energy - the energy supplied was to its own corporate parks which were majorly shut so the consumption was affected. Although partly parks were open for IT people to manage backend infrastructure for company for remote workers. Overall consumption was lower, leading to lower valuation.

Overall, all 3 divisions valuations decreased, leading to decrease in NAV for REIT shareholders. But the some factors improved with time passage from 2020 to 2021 by some extent which has helped increase the NAV from Rs 375/ unit on 31/3/20 to 388/unit 31/3/21 (consolidated).

Financials -

Key ratio -

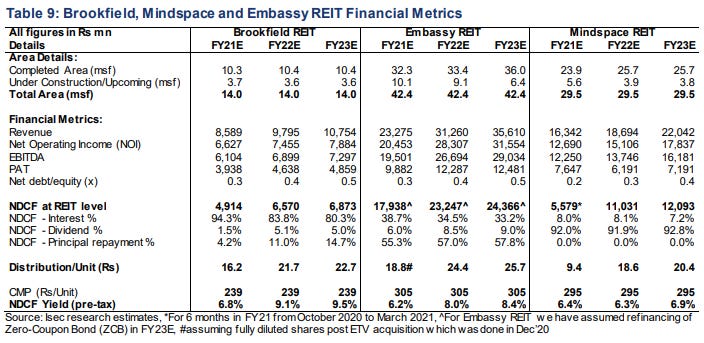

Competitors -

1. Mindspace REIT -

It has 10 properties located in Mumbai, Hyderabad, Pune & Chennai with 31.3 MSF total leasable area & 23.9 MSF completed area. It earns major chunk of revenue from Mumbai(41%), followed by Hyderabad (40%), Pune (16%) & Chennai (3%). The concentration of top 10 tenants is at 37%.

2. Brookfield India real estate trust -

The company has 4 office parks located in – Mumbai, Gurgaon, Noida & Kolkata with total leasable area of 14 MSF (10 MSF completed) with 85% occupancy ratio. It has Right of first refusal over some Brookfield group assets & in some properties has the sole option to purchase 6.7 MSF of property. The top 10 tenants have higher concentration in rentals (76%) due to lower size of leasable area.

Management -

1. Mr. Michael Holland (CEO) –

Mr. Michael Holland holds a Master’s degree in Property Development (Project Management) from South Bank University and is a Fellow of the Royal Institution of Chartered Surveyors. He has over 30 years of experience in the commercial real estate sector in Asia and Europe. Prior to joining the Embassy Group, he was the Chief Executive Officer of Assetz Property Group. He is a Founder of the Jones Lang LaSalle India business, and served as its Country Manager and Managing Director from 1998 to 2002.

2. Mr. Aravind Maiya (CFO) –

Mr. Aravind Maiya holds a Bachelor’s degree in Commerce from Bangalore University, and is an associate member of the Institute of Chartered Accountants of India. He has over 18 years of experience in the field of Finance, Audit, Consulting, Risk Management and Compliance. Prior to joining Embassy REIT, he was associated with BSR & Associates LLP between 2001 to 2019, wherein his last held position was, Partner – Assurance and Audit Services. He specialised in the real estate sector with specific focus on commercial real estate related work during his long stint with BSR. He was also involved in various assignments for the firm, including several capital market transactions, assurance services for several listed companies, leading large audit and assurance assignments as well as strategic initiatives for BSR during his tenure.

3. Mr. Jitendra Virwani (Board of director) –

Mr. Jitendra Virwani is the Chairman and Managing Director the Embassy group of companies, including the Embassy Sponsor. He is also the Founder of the Embassy Sponsor. He has over 25 years of experience in the real estate and property development sector. He is a fellow of the Royal Institution of Chartered Surveyors and a member of the Equestrian Federation of India.

SWOT Analysis

Strength

· Right of first refusal over Embassy properties.

· Strong & professional management team.

· Lower occupancy rates & ability to lease & re-lease properties.

Weakness

· Revenue concentrated in Bangalore market.

· Recently in 2020, REIT’s CFO was transferred to Embassy group.

· No residential property held which have seen increase in rates recently.

· The company needs to pay out 90% of its net distributable cash flows which requires company to take additional debt & equity in order to purchase new property.

Opportunities

· Rising outsourcing trend towards India augurs well for industry.

· Rising flexible work (WeWork) growth in India would be beneficial as promoter family runs WeWork India & has leased from REIT.

Threats

· Embassy group shifting away from office properties post merger with Indiabulls will affect its pipeline.

· Hyderabad/ Telangana is boosting its innovation capacity & has seen lots of corporate moving their base to Telangana.

Risk Reward -

One can try to gauge under/ overvaluation based share price trading at a discount/ premium to NAV. If the discount looks above average (at point A) it might be undervalued compared to point B where it was trading at premium to NAV where it might be overvalued.

The above is just one method to gauge valuation & highly subjective to one’s interpretation. One can also place a bet looking on expected underlying property being undervalued based on one’s own research.

Conclusion -

Embassy REIT is well placed to benefit from increasing startups arising from Bangalore which is also known as “Silicon Valley of India” as the revenue is concentrated from Bangalore. The REIT is well run & has professional management team managing it. The collection efficiency & occupancy ratios are better than peers & also has ROFO over Embassy properties which gives it continuous pipeline of new assets.

Overall, the company looks well placed to benefit from expansion of outsourcing & IT industry boom in India. The point of entry in the stock, the cash flows from properties & the underlying property valuations will ultimately determine investor’s return.

If you liked the article, consider sharing the article & hit the subscribe button below.

Notes -

Company’s management charges fees for managing properties which are described below.

The overall tenure of leases in the Office Parks is typically nine to fifteen years with a three to five years initial commitment period. The lease tenure for City Centre Offices is typically five to nine years with an initial commitment period of three to five years.

As REITs are not high-growth companies, the right valuation metric is dividend yield and how sustainable is the dividend. In overseas markets, that is how REITs are evaluated. You can see the valuation of VNO (Vornado Realty Trust) for instance https://seekingalpha.com/article/4459160-vornado-realty-trust-vno-preferred-shares-safe-not-cheap

Embassy has not paid any dividends so far and it's not clear how sustainable those dividends would be once they begin. Until then, it will be very hard to evaluate a company like this

This all analysis is perfectly ok and has appeared in various fora time and again.

The crucial point is at what price/value, the underlying assets which are earlier "owned" by a builder (in this case by Embassy) are transferred to REIT. Is it at the book value of the developer or something else.

The same is happening wrt to all the REIT/Invits also where the underlying assets are transferred to REIT at a substantial premium to the book value in the guise of "valuation".

Imagine, the developer transferring the assets at book value, then, the entire matrix of return and all other parameters will go a huge change.

Please elaborate on this.