Banking & PSU Fund - Can You Bank On It?

Banking & PSU Fund - Can You Bank On It?

MF shots (Part 13)- is an exclusive series of article which will try to explain in each category of mutual fund. This article focuses on banking & PSU fund category.

Overview -

MF shots - name describes itself where Mutual Fund categories are explained in a brief manner to avoid clutter of information. The current article is continuation of MF shots series by Cellestial Wealth. Previously I have written about short term & medium term debt mutual funds of which can be found by clicking on each category. Each article takes less than 6 minutes but states a few key pointers to be looked upon when choosing a category.

Overnight fund – invests in securities with maturity of 1 day.

Liquid fund – invests in securities with maturity of 91 days.

Ultra short duration funds – invests in securities with maturity of 3-6 months

Low duration funds - invests in securities with maturity of 6 months to 1 year.

Money market funds - invest in securities with maturity upto 1 year.

Short duration funds - invest in securities with maturity ranging from 1 to 3 years.

Medium duration funds - invest in securities with maturity ranging from 3-4 years.

Medium to Long Duration funds - invest in securities with maturity ranging from 4-7 years.

Long duration funds - invest in security with maturity of more than 7 years.

Dynamic Bond funds - invests in securities with varying maturities.

Corporate bond fund - invests in corporate & government securities with varying maturities.

Credit risk fund - invests in corporate securities with no credit rating restriction.

Brief –

It is a unique category as it can invest in central government issued debt, municipal debt issuances, PSU companies & banks. Also, the category allows 20% investment in companies other than mentioned above. The reason behind the category creation seems to be focus towards capital protection with returns similar/ slightly higher than provided by fixed deposits.

Investment objective –

The investments are made in banks, PSU’s & municipal issues with a minimum threshold of 80% to be maintained throughout the period. The sovereign securities provide capital protection while few private banks provide some yield enhancement over sovereign securities.

Suitable for which type of goals –

Goals which are 2-3 years away are suitable for the category.

What parameters to check ?

1. Exposure to risky municipal bonds –

Municipal bonds carry higher credit risk compared to central government & have lower liquidity compared to central government securities in India. Hence, too high exposure to municipal securities in a fund isn’t preferrable.

2. Investment in government owned companies versus private banks –

Private banks offer higher yield but also carry higher credit risk. Defaults can occur in the private banks & 20% allocation to other companies than banking & PSU category where investors would lose money as was the case with Yes bank investors recently.

3. Expense ratio –

The returns from the category are similar for 5 years. Hence higher expense ratio would reduce investor returns. Hence, one needs to keep a watch on it.

4. Portfolio duration –

The rising interest scenario (currently we are in) requires fund manager to invest in lower duration security in order to reduce losses due to lower yield. Hence a lower portfolio duration is preferred in increasing interest rate environment & vice -a-versa for falling interest rate environment.

Interesting insights –

1. Majority of funds in the category have 60-80% of their investments in PSU’s or government securities.

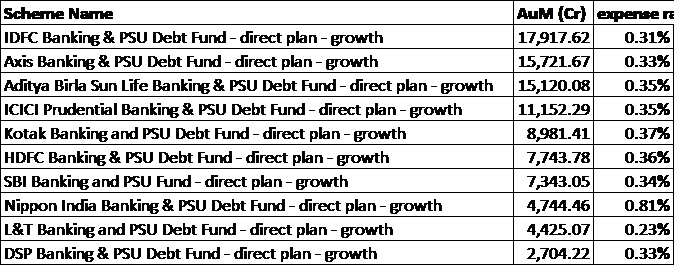

2. Average expense ratio of category is 0.36%

3. Majority of funds have reduced their portfolio duration in expectation of increase in interest rates

4. Baroda BNP Paribas has highest expense ratio of 1.78%

5. Top 10 funds by AUM in the category account for 94% of AUM

Conclusion –

The category is popular with investors as Rs. 100,000 crore AUM is invested in the category. It invests in high investment grade categories given the sovereign ownership or tight regulation norms stipulated by RBI. The past returns from the category are similar with deviation of +/- 1% amongst funds reflecting the limited opportunity set availability. One could look to invest in the category given one’s time horizon is 2-3 years in a fund with reasonable expense ratio.

Overall, Axis banking & debt fund look good given the high AUM, moderate expense ratio & low portfolio duration of 0.72. Also, the funds invested in various companies seems to be appropriately tailored towards the goal of capital protection with returns similar/ slightly higher than FD’s.

I am AMFI registered Mutual Fund Distributor . In case you have mutual fund queries or would like to invest in mutual funds, let me know on my Email - chirag.jain48@yahoo.com or +91-7567473055.

AMFI registration number - ARN-187955

Notes -

Complete data sheet can be accessed here.

Top 10 funds by highest AUM -

Top 10 funds by lowest expense ratio