Are Overnight Funds are useless?

Are Overnight Funds are useless?

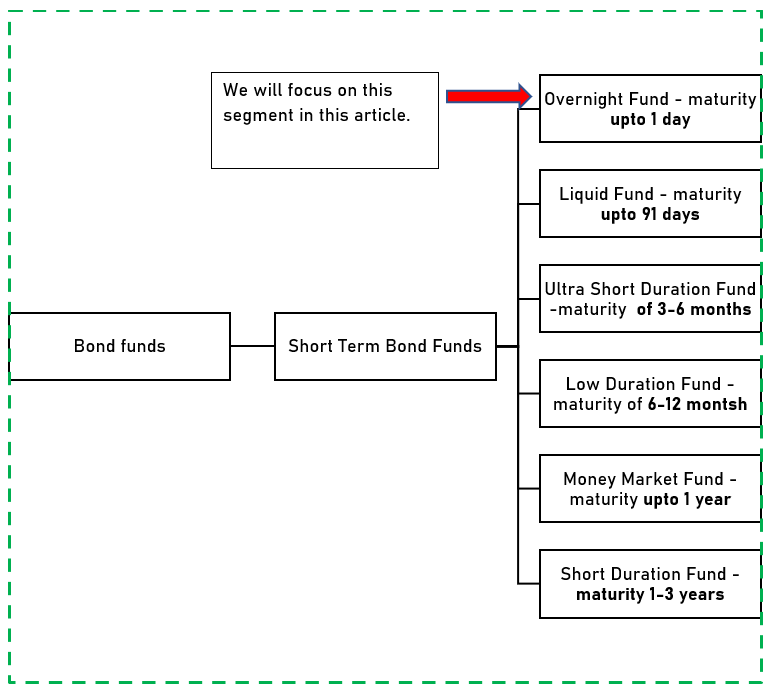

This article is Part 1 of short term bond funds category. This article describes investment objectives, pros & cons of overnight funds. The final section of article compares various overnight funds.

Estimated time read - 7 minutes

In my previous article, I categorized debt, equity & hybrid mutual funds. As many would find various categories of debt mutual funds similar to each other, the series of articles will goes a step further to simplify the complex looking debt funds sector by looking at each sub category under mutual funds & debunk various myths along with. In case you missed out on my previous article, you can read it here.

Due to many sub-categories present in the short term bond mutual fund, each category will be described in a separate article. This article solely focuses on overnight mutual funds. So let’s start right away –

A. Overnight Fund –

Investment objective -

To invest in bonds which have maturities upto 1 day.

Suitable for which type of goals?

Emergency funds for 1 month.

Other short term goals with time horizon less than 1 month.

Risk Level of overnight funds

Majorly, these funds invest in government securities or trade with parties such as Banks, with government securities being collateral & carry the lowest risk due to government securities being collateral.

How to filter between various available funds?

One should not solely look at past returns while deciding the mutual funds. The parameters to be looked upon in a overnight fund are –

i. Portfolio of securities held

One should check whether the securities held in portfolio are backed by the government or issued by corporates with good track record of repayment & credit rating. The transactions done by Banks/ NBFC’s/ other companies in government security as backing is known as TREPS.

ii. Current & past credit rating of portfolio companies

The credit rating reports of companies held in portfolio of overnight funds are available free of cost to investors on google. One can read them & then one can make decision on the riskiness of company.

iii. Comparing returns across different overnight funds

If one sees very high return difference between funds, it should be investigated whether the fund is taking higher risk than it should take.

iv. Expense ratio

Usually the lower the better, wherever the securities being managed are a commodity. (expense ratio means - how much % of your investment value is being charged by the fund management company to cover their cost of managing portfolios.)

Which funds did I shortlist & reasoning behind them?

Out of total universe of 30 overnight funds, the first filter was to sort by mutual fund expense ratio. Next, was to sort by AUM highest to lowest. The filtered out results gave 2 funds which have combination of low expense ratio & AUM (Assets Under Management in the scheme) in top 10 in overnight funds.

Shortlisted Funds -

The next step was to check these funds further –

1. UTI overnight fund –

i. Portfolio holdings -

It has invested 100% in TREPS. (i.e. portfolio of government securities as backing)

ii. Risk levels of portfolio -

So, it holds government securities it has less risk involved.

iii. Returns -

It has similar returns to other funds & has 3.17% Yield to Maturity. (i.e. if one invests today one will receive 3.17% yearly return)

(Source - Valueresearch, As on 4-9-2021)

2. Axis overnight fund –

i. Portfolio holdings -

It’s factsheet of 2021 states it has invested in net current assets but the assets aren’t described further. I enquired to their customer care, but no clarity was obtained (will update as soon as I receive response from Axis MF).

ii. Risk levels of portfolio -

No clarity yet.

iii. Returns -

It has similar returns to other funds & has 3.20% Yield to Maturity.

(Source - Valueresearch, fund factsheet As on 4-9-2021)

Conclusion –

Currently, based on available data, the money kept in savings account yields less returns than investing in overnight fund for a investor whose portfolio size is less than 50 Lakhs. The UTI overnight fund yields net 3.11% ( 3.17% - 0.06%) to investor which is just marginally better than savings account interest rates of HDFC & ICICI Bank. A better option is to keep money in these banks as the return difference is only marginal.

The concluding that question that arises is -

“Why people pay 0.06% expense ratio for 0.11% outperformance net & reduced with rising expense ratios of other mutual funds?”

If you are able to justify it, let me know your thoughts by clicking the button below.

Notes -

The link to data of all available overnight fund can be downloaded here.

Top 10 in Overnight fund category by Lowest expense ratio -

(Source - Moneycontrol & Valueresearch)

Top 10 in Overnight fund category by AuM -

(Source - Moneycontrol & Valueresearch)

Don’t forget to bookmark this page for your future reference & if you liked it, share it now.

In following articles we will focus on each of these debt sub categories –

A. Liquid Fund –

B. Ultra Short Duration Fund –

C. Low Duration Fund –

D. Money Market Fund –

E. Short Duration Fund –